The Blockchain Boom

Ready or not, blockchain technology is turning the world on its head—in the best and most mind-bending ways possible

By the time this article goes to print, hundreds if not thousands of headlines will likely be written at lightning speed about a new breakthrough in blockchain technology. Or a glitch in the latest cryptocurrency trading platform. Or the record-breaking sale of a non-fungible token (NFT) of a one-of-a-kind digital cat on something called Ethereum. Is your head spinning yet? Consider yourself in good company.

It has become almost a cliche to admit you have no idea what any of these words—seemingly coined by a community of elite tech insiders who regularly convene in some alternate universe—mean. But, the era of ignorance is over. Blockchain technology—and the masterminds behind its meteoric rise over the last decade—is in the process of disrupting, dismantling, reimagining, and reconfiguring everything we know about, well, everything. And Pepperdine is jumping into the fray with an innovative academic initiative to propel the University into leadership in the space. So, what is blockchain, who is behind it, and why should we care about the trillion-dollar industry nobody can quite wrap their heads around?

Blockchain 101

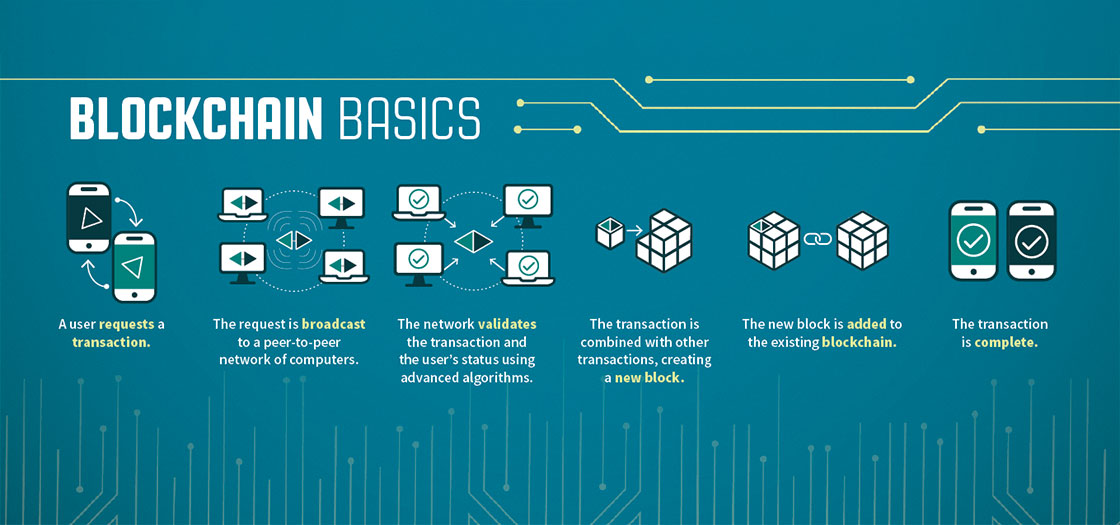

At its core, the blockchain can be simplified as a digital platform that maintains a ledger of transactions shared across a decentralized network. This ledger holds an immutable history of digital transactions—most notably of cryptocurrencies or encrypted digital assets such as Bitcoin—that are legitimized by peer-to-peer consensus. Blockchains are built on open source software, which allows developers to ensure the safety and security of transactions by avoiding third-party governance and interference by a central authority. The blockchain operates on a network of computers that contains a universal data set that is displayed to all users, making all activity, especially the transaction history of digital assets, transparent and unalterable.

One publication compares blockchain to Google Docs, living documents that are created and owned by one party and distributed (not copied or transferred) to any number of people who all have access to the document. Users are able to make changes at their convenience without restriction, and all changes are recorded and visible to all users, making it an entirely transparent process.

Blockchains are made up of multiple individual blocks (think of them as links in a chain) that contain all of the data related to a digital transaction. Each block also contains a 32-bit number called a nonce—an abbreviation for “number only used once”—that is randomly generated when a block is created and a cryptographic hash, a 256-bit number that acts as the block’s digital signature or fingerprint. As blocks—which are stored chronologically—are added to the blockchain, they create unbreakable bonds that are difficult and almost impossible to manipulate.

“No individual party can change the rules or take over the database structure and alter it,” says Thomas Lombardi (MBA ’07), adjunct professor of digital asset finance at the Graziadio Business School and managing director of 3iQ Corp, an investment fund manager offering digital asset investment products such as the Bitcoin Fund. “It would require nation states to invest potentially hundreds of billions of dollars to burn it down. No other party in the world could do anything to these structures.”

Bit by Bit

For a culture so accustomed to relying on major institutions to manage our most valuable assets, it’s no wonder decentralized systems are taking time to catch on. However, the promise of cryptocurrencies and their ability to enable the transfer of funds directly between two parties without the need for a financial institution is appealing to many. It is also the biggest threat to the financial sector, which is heavily regulated by the government.

The strongest thesis within the blockchain and Bitcoin conversation, says Lombardi, is financial inclusion as it relates to currency transactions.

“The privileged few that live in well-to-do areas have access to Venmo and PayPal and the most trusted financial institutions in the world,” he explains. “But that is not the case for 4 billion other people. This technology enables financial inclusion for those who don’t have trust in their government and financial institutions.”

Lombardi cites Etsy, a web marketplace where designers and creators sell handmade or curated items to users anywhere in the world, as an environment that limits the availability and equality of opportunities for merchants to access financial services.

“The reality is that many international sellers have to go through a lot to get the money from their sale,” he says. “They are either making the transaction through their local Western Union that’s connected to a local bank or they have to go through government-controlled banks. Etsy also takes a cut of their profits. You don’t realize how many layers these sellers in different parts of the world have to go through to access their finances.”

Blockchain technology and digital assets such as Bitcoin enable financial inclusion between someone in one of the world’s biggest metropolises and someone operating a business from the most remote, rural region on the other side of the world. But, with the current structure of international banks and tariffs, the possibilities are slim.

So, what does the future of open financial systems look like and what does it enable? So much, says Lombardi. “We use so many intimate products and services in our daily lives such as email, social media, and payments that we have no control over,” he says. “By having this secure database—this open financial platform that no one can manipulate—blockchains unlock so much opportunity for personal rights, free speech, and entrepreneurship.”

Blockchain is the foundation of cryptocurrency, digital assets that can be traded for goods or services through secure online transactions across the blockchain network. Bitcoin, the first cryptocurrency and the longest-running blockchain, was created in direct response to the Great Recession in 2008.

“Bitcoin proved for the first time that you could have an asset that is purely digital in nature,” says Lexy Prodromos (’16), who has been immersed in the world of blockchain professionally since graduating from Pepperdine. Prodromos is currently a product manager for blockchain and digital currency for Discover Financial Services based in Chicago. “Bitcoin is composed of several lines of code and has real value that isn’t backed by gold or currency, and the price is market determined. It was the first proof that you can have something fully digital like this that can be scarce.”

Bitcoin, like gold, is “mined” and exists infinite supply. But unlike gold’s physical extraction from the earth, the digital currency is sourced through a computer. With only 21 million Bitcoin in circulation, a figure determined by its creator, Satoshi Nakamoto, its scarcity model ensures that it remains valuable for an indefinite period of time.

“The way the blockchain is designed for Bitcoin and many other cryptocurrencies is that there are more efforts to secure mining than there are to duplicate these bitcoins,” Prodromos continues. “That was a game changer in allowing you to not only transact these cryptocurrencies peer-to-peer online, but to use blockchain technology to transact purely digital items that have value with people you know and don’t know across the world.”

Policy Innovation

Around 2015 cryptocurrency companies were required to obtain a license to operate virtual currency business activities in their respective cities, an effort to legitimize the elusive nature of the digital transactions. The now-infamous New York-based BitLicense was the only state-recognized business license for virtual currency activities at the time. Prodromos had heard former governor Jack Markell debut the Delaware blockchain initiative at the Consensus conference in New York City. Believing that there might be room for Illinois to form a blockchain initiative of its own, she approached the executives at the newly formed Illinois Department of Innovation and Technology, where they were working on a broader technology initiative and hadn’t fully considered blockchain’s potential in their plans.

Prodromos, who became curious about cryptocurrency and explored it seriously as a career path shortly before graduating from Pepperdine, proposed a plan to the department to develop Chicago and Illinois into national blockchain leaders. This effort helped shape discussions of how to advance blockchain technology in the public sector, which evolved into the Illinois Blockchain Initiative (IBI). At the IBI, Prodromos led education initiatives to raise awareness about blockchain technology; inspire legislation to help Illinois become more welcoming to cryptocurrency entrepreneurs; create a physical convening space where entrepreneurs, students, private businesses, and venture capitalists could build an in-person community to network together; and launch a pilot program to implement blockchain technology within the state government. She is currently the executive director of the Chicago Blockchain Center, a nonprofit organization devoted to the education, promotion, and adoption of cryptocurrencies and blockchain technology. She also supports efforts at the federal level with the Chamber of Digital Commerce, a Washington, DC-based advocacy firm for blockchain and digital currencies.

“Emerging technology and government often give rise to a push and pull between trying to allow innovation to flourish while also protecting citizens from bad actors trying to take advantage of that technology,” Prodromos says. “Especially at the time, there had been several very large Bitcoin and cryptocurrency exchange hacks that had resulted in the loss of millions of dollars. One of the interesting things about cryptocurrency is that, while it inspires personal financial freedom, it also places much more responsibility on the individual to manage their funds.”

Prodromos cites data from a few years ago that estimates that, of the 18 million Bitcoin that have been minted and are in circulation, 4 million to 6 million are missing and permanently inaccessible because of misplaced or forgotten private wallets, unique keys that are used to validate Bitcoin transactions and specifically designed to prevent third parties from using or altering transactions on the blockchain.

“There were reasons at first for governments to be skeptical of Bitcoin technology,” Prodromos says. “At that point in time, Bitcoin was famous for being traded for illicit materials and used in ransomware attacks. What we wanted to do at the Chicago Blockchain Center and Illinois Blockchain Initiative was shine a light on other, noncriminal uses of this technology.”

While the technology is still nascent, Prodromos says that it has the potential to alleviate pain points in many different industries ranging from healthcare, finance, real estate, media, and the arts. One of the pilot programs Prodromos initiated at the IBI was with the Cook County Recorder of Deeds Office in an effort to use a Bitcoin equivalent called colored coins to ascribe land titles and deeds, using blockchain technology to enable traceability and transparency in verifying ownership of land parcels and other forms of property and making the transfer of land ownership easier.

“We have much more clarity now about how this technology can be leveraged and how to keep citizens safe from bad actors,” she says. “Blockchain turns a lot of models on their heads. The technology poses the question: ‘What if we didn’t need third-party intermediaries for digital transactions anywhere?’ Some people say decentralizing isn’t the way to go. In the future, we’re going to approach a world where there’s a mix of certain centralized and decentralized processes that increase security while maintaining the speed and ease of use that certain centralized protocols have right now. Blockchain technology accelerated that and is moving us in the right direction of having much more transparency in a trustless world.”

From Bait to Plate

Much of the mystery surrounding blockchain is related to its inherently concealed nature and distinctive and often puzzling language, which not only intimidates tech novices but also creates confusion and, ultimately, skepticism among the general public. Many wonder how the technology will play a part in their daily lives and processes. While major institutions such as healthcare and higher education have adopted the technology to give individuals access to their own medical records and academic transcripts, blockchain has and will continue to show up in more ways than anyone can imagine.

Throughout the Pacific region, overfishing and illegally harvested fish have resulted in a massive decline in revenue across fisheries. Hundreds of thousands of tons of fish that were procured through unreported and unethical fishing practices cost the industry more than $600 million over a five-year period in the last decade. Beyond patrolling waters and implementing stricter fish-trafficking laws, the World Wildlife Federation has partnered with a blockchain venture to create transparency around fish sourcing all the way through the supply chain.

“Through blockchain technology, you can track a piece of tuna from the moment the catch comes in to when it lands on your plate,” Lombardi says. “The tuna fillet delivered to your house even comes with a picture of the fish it came from.”

Specific data-collecting processes, often referred to as data provenance, essentially an audit of how data was collected and used, tags and tracks each fish as it travels from the fisherman, to the processing plant, to the packaging and distribution facility, to the retail establishment, and, finally, to the consumer. The consumer can then scan a QR code and see every step of the process using a blockchain database.

The benefits to the supplier are a deeper analysis of their supply chain and more precise quality control. To the consumer, this level of transparency affirms their purchasing choices and their confidence in buying from ethical and sustainable producers. Most importantly, tracking the origins of responsibly sourced products is a major factor in combating and eliminating greenwashing across industries that manipulates and misleads consumers into believing a product is more environmentally friendly than it is.

“In the case of product labeling, we have to trust someone to tell us that the product was responsibly sourced. A third party sits in the middle and claims a product’s validity,” says Lombardi. “Let’s actually just use data. Let’s hold people and companies responsible. We don’t need anyone to tell us what we’re consuming is responsibly sourced. We can find out where things actually came from and make the best decisions for ourselves based on actual data.”

By the Same Token

Beyond the impact of blockchain technology on the industries that shape the world around us, many individuals—especially artists and content creators—have found greater opportunities to permanently secure their ownership and the authenticity of their work. Artists and musicians across mediums are using blockchain technology to expand their creative opportunities with NFTs, unique and irreplaceable collectible tokens ascribed to their digital art that live on the blockchain. An NFT’s value is determined by its popularity, and it can be sold by the individual through the exchange of cryptocurrencies. In March 2021, the auction house Christie’s made history with the $69 million sale of the first NFT based on a digital work of art.

In the music industry, artists associate NFT technology with two functional areas: the sale of a collectible audio clip and the authenticity of ownership and copyright. While anyone can copy and listen to the audio, music NFTs, in essence collectible editions of music, can attribute initial ownership to an individual and offer owners provenance—the digital verification of ownership.

NFTs of digital art and music are generally owned by one person who is listed on the blockchain ledger as the owner, but most people can still access the content. The sale of ownership and copyright is what raises legal concerns about owners’ rights. For example, if an owner sells 10 percent of a copyright, does that mean the purchaser is entitled to future income as well?

To combat these concerns, creators can build separate income streams into a smart contract—a transaction protocol stored on the blockchain that is automatically executed or documented when the terms of an agreement between parties are met—but the question remains if purchasers are entitled to profits from subsequent sales of the NFT.

One challenge that music industry insiders predict is the possibility of an NFT owner infringing on a creator’s original work. In some cases, the person minting a musical work does not own the song to mint it in the first place, and if the creator does not catch the minting of the NFT in time, it can be difficult to prevent and correct it. Another challenge is the currently undetermined extent of an NFT owner’s right to grant derivative licenses, such as to allow a major television network the right to use the music in the NFT.

While these practical concerns are emergent, their legal implications are not novel.

The successful adoption of blockchain technology in the world of art, music,

and collectibles depends on the industry’s efforts to develop norms to help govern

and guide these processes, especially as they relate to the sale of a copyright and

the attachment of contractual rights with the blockchain. As more artists use NFTs

to connect with audiences directly, manage their identities, and simplify transactions

of their work, industry professionals remain optimistic about the emergence and prominence

of NFTs and are equipped with a general understanding of blockchain technology and

the challenges and opportunities it brings—a good sign for the overall health of the

industry.

In the Classroom

In 2017 Lene Martin (EdD ’16, PhD ’21) became interested in the applications of blockchain in higher education. The founder and CEO of Coastline Consultancy Inc., a firm that offers consulting services in media and emerging technologies, Martin was advising in the field of organizational development for one of the first public blockchain companies. At the same time, she was working as the information security communication lead at Amgen running the biotechnology company’s global cybersecurity communications, including efforts to educate on blockchain for healthcare.

She began thinking of ways blockchain could contribute to autonomy and accountability in the world of healthcare and considered the ways the technology could put more resources and opportunities in the hands of individuals. “It can certainly do that through cryptocurrencies, but it can also do that just by giving people access to their own healthcare records,” Martin says. “That’s when I fell in love with it. I kept thinking about all of the possibilities blockchain could bring to people around the world.”

An alumna of the organizational leadership doctoral program at the Graduate School of Education and Psychology and at the time a current student in the school’s global leadership and change doctoral program, Martin considered the value of bringing blockchain to Pepperdine. She applied for and won a Waves of Innovation grant in 2019 to create Blockchain at Pepperdine, an interdisciplinary and inclusive initiative designed to advance blockchain technology and innovation at the University. Blockchain at Pepperdine comprises a sophisticated team of academic and industry advisors and serves as a resource for blockchain conferences, curricula, certificates, collaboratories, and consulting for students, faculty, staff, alumni, and the community. To date, Blockchain at Pepperdine has developed three University-wide events, including multiple workshops and seminars, five master’s-level courses with blockchain concentrations, professional executive certificates with technical and nontechnical tracks, countless presentations and consultations both internal and external to the University, and more than 16 solution-design papers with several in progress.

In Martin’s blockchain business applications and analytics course at the Graziadio Business School, students learn about blockchain foundations before jumping into a deeper study of blockchain applications and analytics over a seven-week period. The course encourages students to determine a real-world issue and takes them through the lifecycle of a blockchain project focusing on decentralized applications such as smart contracts or NFTs as part of that solution.

Students also have the opportunity to partner with existing companies in the industry as they engage in discovery analysis, design mapping, and creating user-journey flows that go through layers of functional and technical requirements. By the end of the seven-week course, students have developed the wireframe of an actual application for their smartphone. Martin shares that if the course were spread over 14 weeks, students would, by the end of it, be able to develop a minimum viable product—the early form of a product that contains enough features to deliver a usable experience to customers.

“Students often complete the course wondering what they can do next,” Martin says. “They’re wildly excited about it. Some of them have wanted to transition careers after taking the course. Some of them have established themselves as blockchain experts at work. And, for many, it’s become their favorite class. We’ve been thrilled with that response.”

A New Digital Generation

As blockchain technology finds its legs in the mainstream, graduating students are entering the workforce and discovering career opportunities in an emerging field with great promise. While more seasoned professionals are having to pivot and reimagine existing and deeply established processes, this new crop of graduates is blazing into blockchain with an energy—and opportunities—rarely seen before.

Zayi Reyes (’17), who graduated with a degree in integrated marketing communication from Seaver College, was pursuing marketing and advertising opportunities when a friend recommended her for a role at a company called MetaX in Santa Monica, California. The startup that, at the time, employed just a handful of people, was an advertising technology company staffed with developers who were considering the ways blockchain technology could remedy the digital advertising industry’s fundamental flaws, namely fraudulent transactions during the exchange of billions of dollars. Reyes became deeply involved in the burgeoning company’s operations and admits to being thrown into a master class in blockchain’s opportunities in advertising.

When MetaX partnered with Consensus, one of the biggest blockchain incubator companies at the time, Reyes took a deeper dive into the technology. She was hired a few weeks before the company launched their own token, then one of the first American-based tokens, and raised $10 million in 23 seconds. Reyes was hired to manage the marketing strategy in the tech markets.

“I had no idea what I was getting myself into, but I’m so glad I did,” says Reyes. “That experience completely changed my life.”

Reyes currently works for Unstoppable Domains, the leading blockchain domain registry, that enables users to build decentralized websites that simplify cryptocurrency payments. The company offers users domain names (for example, pepperdine.crypto) that act as cryptocurrency wallet addresses that can be used to send and receive hundreds of cryptocurrencies across more than 50 wallets, exchanges, and applications around the world. This product solves incorrect cryptocurrency transfers that are common within the crypto industry due to long, complex addresses that are necessary to use for crypto payments. These mistakes can result in a permanent loss of funds. Reyes is involved in partnerships and marketing and works with the biggest crypto content creators in the world to share the value of Unstoppable Domains with their massive social media communities.

“When I first started doing this, nobody had really thought about content creators in the crypto space because it was so new,” says Reyes. “And there’s also a kind of unwritten rule in crypto that you don’t market it. Now, you’re seeing companies hire performance marketing teams to run ads and secure sponsorships. As projects learn to accept marketing, I’m seeing a rise in companies being invited to podcasts and creating large amounts of educational content, especially on social media platforms like TikTok.”

Blockchain, while it has been around in various formats since the early 2000s, is still in its infancy as far as larger industries are concerned. Because of its nascency, blockchain has provided professionals who entered the field just a year or two ago with opportunities to grow significantly in their careers in a short period of time.

“Regardless of your age or background, you can make a name for yourself in the industry and become an expert because it’s just so new,” says Reyes, who is a dedicated advocate for women and Latinas in tech. She and her colleague presented at South by Southwest 2021 on how decentralized autonomous organizations are built on the blockchain and operate in a self-governed manner. Reyes was also recently named a delegate of the National Briefing of Women of Color in Blockchain. “If I had gotten my start in any other industry, I would have been starting in entry-level positions and spending years working my way up. Because I entered the blockchain industry when I did, I’m running my own department. I’m getting opportunities to represent my company in front of major audiences. It’s so exciting how much opportunity there is.”